For purposes of this Guide Article, you exchange inventory when either:

- You return one or more previously purchased inventory items to a supplier and receive different inventory items from the supplier, or

- A customer returns one or more previously sold inventory items to you and receives different inventory items from you,

and no credit is involved in the transaction. That means:

- Neither Accounts receivable from a customer nor Accounts payable to a supplier is adjusted, and

- No credit or debit note is involved.

In other words, an exchange occurs when all movement of funds and inventory is accomplished in a single transaction. If the items exchanged are not of equal value, movement of funds can be via bank or cash transaction. If the customer or supplier will owe money to after the exchange, use a receipt form to record the transaction.

Note

Technically, an exchange can be recorded with a receipt or payment, regardless of whether either party to the transaction owes the other money or who owes money to whom. However, your records will be easier to understand if you use a receipt form when the other party owes you money.

Returning goods to a supplier

Conceptually, exchanging inventory with a supplier is equivalent to you selling back the item(s) you originally purchased from the supplier and buying new item(s) from the supplier. In fact, you could enter two separate transactions. But there is a simpler way that produces identical results.

In the tab, click on :

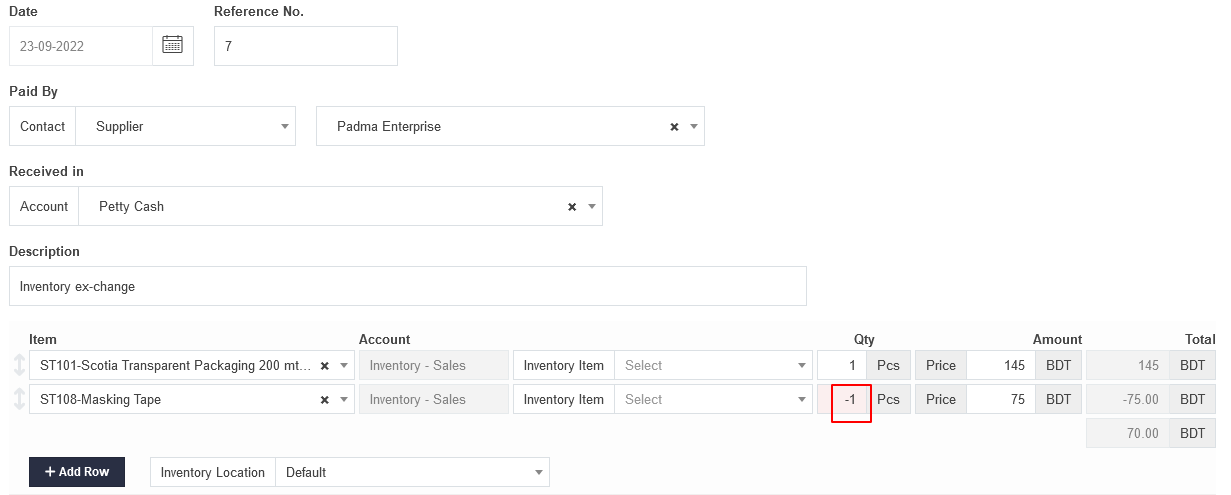

On the receipt form, list all inventory items you are returning to the supplier and their quantities. Include any tax code that was applied to the original sale.

Next, list all inventory items the supplier is furnishing in the exchange and their quantities. Because you are effectively paying money for the replacement item(s) rather than receiving it, enter the replacement quantities as negative numbers. Again, include any applicable tax code.

Click to record the exchange.

Example

ABC Industries previously purchased a Scotia Transparent Packaging Tape from Padma Enterprise. ABC Industries realizes it purchased the wrong product and wants to exchange the Masking Tape. Because these are wholesale transactions, no tax is assessed on any portion of the transaction.

Prior to the exchange, ABC Industries’s list reveals it owns 15 Transparent Tapes and 5 Masking Tapes:

The receipt form is completed as shown below. Note the negative quantity for the replacement item:

Because the returned item is worth more than the replacement item, Edison owes Brilliant 70.00. When the transaction is complete, inventory quantities have been adjusted. Transparent Tape have decreased by 1 and Masking Tape have increased by 1:

Note

If replacement items are worth more than returned items, you will owe the supplier additional money. This will be shown by a negative total. (A negative receipt is the same as a payment.)

Customer returns goods

When a customer exchanges inventory, you are effectively selling replacement items and buying back the items you originally sold. The procedure for recording the transaction is basically the same as the one described above:

- Enter a new receipt to either a cash or bank account.

- Enter returned item(s) you receive with positive quantities.

- Enter replacement item(s) you provide the customer with negative quantities.

- A positive receipt total means the customer owes you additional money. A negative receipt total means you owe the customer money.